One of the biggest retirement mistakes you can make is not realizing what you don’t know. The reality is that most people don’t get good and objective financial advice before they retire.

There are many ways retirement can go wrong.

Here are the Top 10 retirement mistakes and how to avoid them.

Retirement Mistake # 1: Cashing out all from EPF and park into Saving account.

Can you withdraw all your EPF money after age 55?

Technically YES.

However, just because you can withdraw all your money from EPF, does not mean you should.

And, don’t simply keep the money in Savings or Current accounts. Besides the money does not grow, you’ll spend it like water coming out of the tap.

What you can do:

Diversify your retirement fund into a few places. My recommendation is:

10% – for usage in a year (daily commitment)

20% – ASB/ ASW/ Tabung Haji

20% – Principal funds or Unit Trust (with diversified portfolio equity, balance, sukuk)

Plus, if you are healthy at the age of 65, you could live another 20 – 30 years.

One of the biggest retirement mistakes many people make is underestimating the expenses in retirement. Among reasons are;

Ignore the impact of inflation on their expenses

Not knowing the medical cost require later in life

Unplanned big-ticket expenses such as major house repairs, kid’s wedding, etc

What you can do:

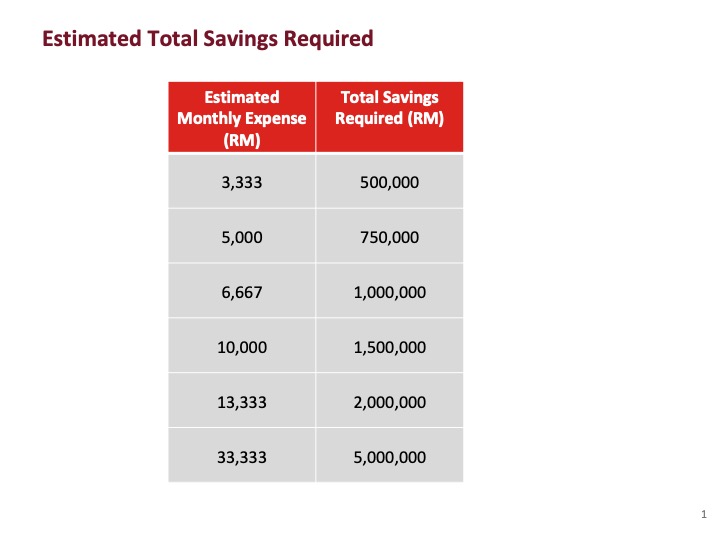

You need to know what your monthly expense after retirement. It shall include food, utilities, health insurance, long-term loan, transport & wants.

Once you’ve determined the monthly expense, then you calculate backward how much savings that you need to build up. eg, if you want to have a $10k monthly expense, then you need to have $1.5 Mil in your total account.

Check below table for the amount of savings you required for monthly expenses.

Retirement Mistakes # 3: Assuming you can work longer

About half of retirees report leaving the workforce earlier than they had planned. Some are lucky as they get company package or windfalls. Many more retire because they lose their job and cannot find a replacement or because of ill health.

As a financial consultant, I met a lot of retirees that have to retire in early 50’s due to office politics, lose job or being retrenched.

What you can do:

No matter how much you want to keep working, it’s no excuse to not save for retirement. Save or invest 10% – 15% of your income for retirement savings.

Retirement Mistake # 4: Spending too much too soon

I understand the temptation. Especially when you see a big sum of money and feel that you deserve to spend it as you have worked all this long. But spending your EPF money without a proper plan is a poor financial decision.

Normally, retirees tend to spend the money on house renovation, travel, kids’ college, kid’s grand wedding, etc. However, spending money you have not budgeted for will eat away your retirement savings quicker than anticipated.

Retirement Mistake # 5: Carrying debt into retirement

Being in debt when there is no steady income is a serious concern. The more debt you have, the quicker you will run out of your retirement savings.

What you can do:

No consumer debt by age 50.

Ie you should not have a personal loan, cash rewards loan, or huge credit card balance.

Stocks are highly volatile and stock prices can fluctuate from one day to the next.

If you invested in higher risk, higher return stocks, they can decline just when you need them. And they may not recover before you exhaust them.

To double your money in a short period by playing the stock, the risk is too high and not worth it. This includes bitcoin, forex trading, multilevel marketing, and skim cepat kaya (rich quick scheme).

What you can do:

Limit the alternative investment by not more than 10%. An alternative investment is other than EPF, ASB, Tabung Haji, FD, bond, and unit trust fund.

If the investment is 10% of your net worth and you lose it, it is still survivable.

Retirement Mistakes # 7: Failing to prepare for medical expenses

Medical cost is not cheap nowadays. Hence, having good medical health insurance is essential. Furthermore, many healthcare expenses, like dental costs, eyeglasses, and hearing aids are often not covered by insurance/takaful.

What you can do:

Ensure healthcare costs and medical card premiums are included in your annual budget.

Keep your body healthy.

Being healthy can save you a lot of money in the future. Eat a healthy diet, be physically active, read and think, quit smoking, sleep enough, etc.

Retirement Mistake # 8: Relying too much on EPF savings

Many people think EPF savings is enough for retirement.

All parents want what’s best for their kids. But you don’t want to exhaust your retirement funds by being too generous to your adult kids. Think long and hard before you contribute towards the down payment of a car or house, grand weddings, etc.

What you can do:

Talk to your kids about their funding options. If they don’t have enough money to pay for their dream car down payment, they might need to look for a smaller car. Or, target with a less expensive home.

As much you want your kids to be successful, there needs to be balanced.

Some of us enjoy collecting stuff. They have more than two cars, motorbikes, expensive watches, branded bags, etc. When you have a lot of stuff, it means you need more storage, you spend more time and money for maintenance and repairs, and more time to clean them.

I often watch the ‘American Pickers’ tv series. Many parents who collect items, ended up their kids don’t want the items and sold them for quick money.

What you can do:

Retirement is an excellent time to simplify your life. You can check what things you really need and want. Maybe you could consider selling some of your unused or collectible items. Use the money towards retirement savings or a fun experience.

Don’t get your heart set on gifting your items to your children. They might have different priorities and do not value them.

Thanks Abdunnajib.

Public mutual is a mutual fund.

So, investment such us Koop or mutual funds, I reckon 20% of EPF money. If adventurous enough, you can extend up to 30%.

Khairul, what u preach is just common sense but unfortunately that sense is not commonly found. Nice of u to tabulate it. I retired at a ripe old age of 56. And at 61 now, l haven’t touch my EPF. Just living off my rental income and other savings.

Wah.. Arshad Ahmad. Alhamdulillah..

That’s truly awesome. Having plan your retirement earlier was really helpful.

Perhaps, if you don’t mind sharing what did you do right , that helps you now.. Looking forward to your response

Different people have different strategy and most importantly different set of circumstance unique to him. I wish l cud share my story with all, but l m just not ready to. All d best bro.

Khairul, what u preach is just common sense but unfortunately that sense is not commonly found. Nice of u to tabulate it. I retired at a ripe old age of 56. And at 61 now, l haven’t touch my EPF. Just living off my rental income and other savings. Need to plan early for comfortable retirement.

Salaam Ramadhan.

Thank you for sharing your thoughts and ideas. I am a government retiree. I find them useful. May Allah bless us all with good health, happiness and prosperity. Meanwhile, eat healthy, exercise and stay safe.

Thank you Daniel for reading and your kind words. Glad that you find it useful.

Wish you a good health and beautiful moments with family, friends and lovely grandkids.

Alhamdulillah Umar. That’s awesome . Glad to know that you’ve settled all the loans and still working. May you have a wonderful journey in future. InsyaAllah

Oh dear Rosita Khan. Although mistakes done, hopefully you’re able to fix and get your financial back in order. Should you need help, do let me know. I can be contacted at 012- 2347400. InsyaAllah

I just retired at 56. I use my money to settle all my debt. Alhamdulillah. Now because of PKP, i stay at home, spending my pencion and let my money in ASB.

Alhamdulillah Shawa. To settle all the debts is indeed a relief feeling..

Tenang je rasa kan :). Wish you a beautiful moment during your retirement . Amin

Should you need any info or help in future, my pleasure to assist. InsyaAllah.

Khairul, 012-23 47400

Everybody need to develop personal FM(Financial Model) using microsoft excel work sheet. Put in all your current & future expences extending to say 85 yrs if yoy are healthy. You can include all calculations in the model. The model will be your health check every time you want to make a major expense decision and any changes along the way. Include everything in the model eg loan repayment, future child education & wedding expenses etc. Also your vacation plan, parent obligation, zakat calculation, infak. For me I developed the model when I started work & keep on polishing it along the way. I am in my forth year retirement now & I never miss updating my daily expenses every night before I go to bed. You can include all auto generated calculations for all your investment div, bonuses, gain & also zakat calculation for all your anual gain. I work in GLC before & we use FM to calculate bidding strategy for big billion dollar investment.

Wow Nik Ahmad Najmi. I’m super impressed.

What you did is detailed process and full of discipline which hardly to find in the ‘rakyat jelata’. I salute you for that 🙂

Glad that you made use the knowledge in your workplace and applied in your personal finance. It’s indeed very helpful in your retirement years. Alhamdulillah..

Hi Khairul,

Great piece of article.

What’s your view of investing all your EPF savings into buying a property? Lot’s of lelong (option) property nowadays.

Thanks so much ST for your kind words. I truly appreciate.

Property is another investment for longterm. You hardly can monetise the investment in short period. From my experience of having a few properties, it also has it’s own challenges. Hence, you need to do a lot of homework before purchase any property.

Don’t invest all your EPF money into a single property. If it happen to be a bad property, you will end up stuck with it for a long period. And you have no money to spend for daily usage.

I reckon to diversify your epf money. property can be about 20% from EPF savings.

Thank you again for your opinion. If just investing 20% of EPF to purchase a property, it’s not going to be much. Furthermore, if we reach 55, bank loan might not be possible.

What’s your view?

Do you mind if I call you personally for your advice?

Berbaloi membaca. Saya berpendapat alangkah bagus sekiranya kita dapat membuat investment yg membolehkan kita mendapat pulangan yg mencukupi bagi monthly expenses. Wujudkah skim2 seumpamanya ? Apa pendpt tuan.

Terima kaseh Zulkifli kerana luangkan masa untuk membaca. Saya sangat hargai.

Saya cadangkan investment di tempat yang stabil seperti ASB, unit trust, Koop , ASW. InsyaAllah , capital nyer terjaga dan pulangan yang sihat.

Jika ingin invest di unit trust, saya sangat suka investment secara bulanan. Ia kurang risiko, pulangan yang sangat bagus dan bole membina asset across time. InsyaAllah

Is it wise to pay off all my housing loan while the interest rate is low.

The rentals all cover my instalments.. I’m thinking of buying another property from my EPF..

Wah.. Mohd Fauzi ni memang suka property ya 🙂

This is my view.

If the house loan is for your own stay, then it’s ok to pay off the debt.

But, if the house is for investment, and the loans are paid by the tenants, then not necessarily. It’s good to have cash for future opportunities .

If you want buy another property, I reckon 20-30% of your EPF money.

Excellent read. Too bad way too many malaysians are not aware on how to save properly. Perhaps because there is no financial planning education in school or colleges. I’m late 30s and InsyaAllah will be able to save around 2m (1m epf n 1m savings) in about 4 years time. By the time i retire i shud be able to save around 12m. However I’m not sure whether i really need that much money. Maybe i shud retire earlier once i have around 5m in savings n spend the rest of my life study important things like religion n philosophy. I’m also quite frugal n don’t really like fancy car. My Proton Exora is more than enough for me n my family. In the current economic situation, there is no job security n that’s one of the reason why we really need to live within our means, plus having 10-15% saving is crucial.

Thanks for sharing your story Hamba Allah.

You are successful in your career as well as in your financial. Indeed you’re a young millionaire. Alhamdulillah.

I love your principle. Knowledge is more important than those fancy stuff. A good example to our community.

Wasalam Rozita,

My view, priority shall be you to have your own medical card. At least, less worry of your health during retirement. Then, only for your kids.

Take care of yourself first. It will put you in a better position to support those around you. InsyaAllah

Salam Khairul,

Based on our communication, at least I have the comfort that I am on right track and financially healthy in my retirement age now. Keep up the good work and bakti.

Assalamulaikum khairul. Terima kasih dengan info yg diberi. At least Ada jgk panduan utk Saya@kita utk Masa Akan datang.. masih berbakti kurang 20 thn lagi utk bersara, in shaa Allah.. Akan dilaksanakn mengikut perancangan.. terima kasih..

Waalaikumsalam Muhamad Ismail,

Syukur sedikit sebanyak tulisan ini memberi faedah kepada Muhamad Ismail dan pembaca lain. Alhamdulillah.

Jika ingin lebih informasi dan pertolongan untuk merancang kewangan, saya sedia membantu. InsyaAllah.

Salam Ramadhan.

Good advice. What about buying a house. Buy cash using half of your EPF. House price normally increases over time. If you need money one day, sell it off.

Thanks Nazri.

Buying house for investment has it’s own challenges. With current housing price, it might and might not increase after a few years. Many factors to consider before buying a house, such as location, maintenance, impact of mistakes etc. Plus, investment in a house is not as liquid as ASB, ASW or unit trust.

If you want to buy a house, I recommend to use 20% of your EPF money.

Thanks Nazri.

Buying house for investment has it’s own challenges. With current housing price, it might and might not increase after a few years. Many factors to consider before buying a house, such as location, maintenance, impact of mistakes etc. Plus, investment in a house is not as liquid as ASB, ASW or unit trust.

If you want to buy a house, I recommend to use 20% of your EPF money.

Alhamdulillah. Great to read it as I’m reaching near 55yrs and still thinking what to do with the $. Thank you for sharing and will contact you personally for some advise in shaa Allah

Terima kaseh Nor Azizah. I’m happy to know that this article gives a bit guideline to you and the readers. Alhamdulillah.

Ada rezeki in future, kita jumpa. InsyaAllah.

Salam khairul,

Tq for great tips, anyway as a muslim we should not too worry about the money, we should allocate certain % of the saving for infaq/sadakah for jariah.

Wasalam Mohamad,

Indeed true . Tangan yang memberi lebih baik dari yang menerima. When we take care of ourselves, we can provide better for the people around us. InsyaAllah.

someone approach me to invest in Islamic redeemable preference shares which gives out 12%pa

That’s seems like safe & comfortable investment do you think?

Thanks Fauzi for a great question.

My view:

1. Redeemable preferences shares (RPS) can be seen like a bond or fixed income. It pays dividend but no capital gain.

2. Instead of taking loans, company issue RPS to raise money.

3. Question to ponder: With current borrowing rate is so low at 4%, why the company would want to issue RPS and pays dividend at 12% pa?

Thanks Khairul for shared your though. I just reached 55 last month. What’s your opinion if I just let my saving inside epf instead of invest in ASB, ASW or mutual fund. Might be I just need to transfer some amount into THaji. For info, I plan to continue working for next 3 years.

Alhamdulillah.. Kalau ada rezeki untuk bekerja, teruskan. Till age 60 pun ok 🙂

And you can leave your money in EFP without needing to transfer them. If you do that, then every year just withdraw about 5-7% of your total epf money.

InsyaAllah, the EPF money will last you for many many years.

Khairul. I like your preach as it goes well with mine too. Your opinion were more realistic in today’s financial challenge. Keep it up!

Thanks Shamsul for the support and kind words. And for you to comment here, means a lot to me. Thanks again.

What is other investment like Kooperasi own at Malakat Mall. Public mutual

Thanks Abdunnajib.

Public mutual is a mutual fund.

So, investment such us Koop or mutual funds, I reckon 20% of EPF money. If adventurous enough, you can extend up to 30%.

Khairul, what u preach is just common sense but unfortunately that sense is not commonly found. Nice of u to tabulate it. I retired at a ripe old age of 56. And at 61 now, l haven’t touch my EPF. Just living off my rental income and other savings.

Wah.. Arshad Ahmad. Alhamdulillah..

That’s truly awesome. Having plan your retirement earlier was really helpful.

Perhaps, if you don’t mind sharing what did you do right , that helps you now.. Looking forward to your response

Different people have different strategy and most importantly different set of circumstance unique to him. I wish l cud share my story with all, but l m just not ready to. All d best bro.

Noted Arshad Ahmad. InsyaAllah in future.

Salam Ramadhan.

Khairul, what u preach is just common sense but unfortunately that sense is not commonly found. Nice of u to tabulate it. I retired at a ripe old age of 56. And at 61 now, l haven’t touch my EPF. Just living off my rental income and other savings. Need to plan early for comfortable retirement.

Indeed true Arshad Ahmad. The earlier we plan, the more comfortable is our life. InsyaAllah.

Salaam Ramadhan.

Thank you for sharing your thoughts and ideas. I am a government retiree. I find them useful. May Allah bless us all with good health, happiness and prosperity. Meanwhile, eat healthy, exercise and stay safe.

Thank you Daniel for reading and your kind words. Glad that you find it useful.

Wish you a good health and beautiful moments with family, friends and lovely grandkids.

Good advise Mr Khairul. At 56 years old, i had only withdrawn 10% of my EPF to settle my loan. Alhamdulillah I am still working.

Alhamdulillah Umar. That’s awesome . Glad to know that you’ve settled all the loans and still working. May you have a wonderful journey in future. InsyaAllah

This is really helpful. I hv done almost all of those mistakes, except i dont spend it on my kids (dont have any) but my mother.

Oh dear Rosita Khan. Although mistakes done, hopefully you’re able to fix and get your financial back in order. Should you need help, do let me know. I can be contacted at 012- 2347400. InsyaAllah

Great to have this, bro.

Keep it up 👍

Thanks so much Dzuhrimohd. Truly appreciate your feedback .

btw, I pompuan hehehe

Awesome advice…

Terima kaseh Awang. Alhamdulillah . Glad that you find it useful.

I just retired at 56. I use my money to settle all my debt. Alhamdulillah. Now because of PKP, i stay at home, spending my pencion and let my money in ASB.

Alhamdulillah Shawa. To settle all the debts is indeed a relief feeling..

Tenang je rasa kan :). Wish you a beautiful moment during your retirement . Amin

Should you need any info or help in future, my pleasure to assist. InsyaAllah.

Khairul, 012-23 47400

Everybody need to develop personal FM(Financial Model) using microsoft excel work sheet. Put in all your current & future expences extending to say 85 yrs if yoy are healthy. You can include all calculations in the model. The model will be your health check every time you want to make a major expense decision and any changes along the way. Include everything in the model eg loan repayment, future child education & wedding expenses etc. Also your vacation plan, parent obligation, zakat calculation, infak. For me I developed the model when I started work & keep on polishing it along the way. I am in my forth year retirement now & I never miss updating my daily expenses every night before I go to bed. You can include all auto generated calculations for all your investment div, bonuses, gain & also zakat calculation for all your anual gain. I work in GLC before & we use FM to calculate bidding strategy for big billion dollar investment.

Wow Nik Ahmad Najmi. I’m super impressed.

What you did is detailed process and full of discipline which hardly to find in the ‘rakyat jelata’. I salute you for that 🙂

Glad that you made use the knowledge in your workplace and applied in your personal finance. It’s indeed very helpful in your retirement years. Alhamdulillah..

how is wish you could share the FM

Hi Khairul,

Great piece of article.

What’s your view of investing all your EPF savings into buying a property? Lot’s of lelong (option) property nowadays.

Thanks so much ST for your kind words. I truly appreciate.

Property is another investment for longterm. You hardly can monetise the investment in short period. From my experience of having a few properties, it also has it’s own challenges. Hence, you need to do a lot of homework before purchase any property.

Don’t invest all your EPF money into a single property. If it happen to be a bad property, you will end up stuck with it for a long period. And you have no money to spend for daily usage.

I reckon to diversify your epf money. property can be about 20% from EPF savings.

Thank you again for your opinion. If just investing 20% of EPF to purchase a property, it’s not going to be much. Furthermore, if we reach 55, bank loan might not be possible.

What’s your view?

Do you mind if I call you personally for your advice?

yes you can call me. My number is 012-234 7400.

Thank you so much. We shall have a chat soon

this is v good

Thanks Farah Farina.. Appreciate it

Very useful and practical financial advice for Malaysian!

Thanks for reading Hisham M. Glad that you find it useful.

Alhamdulillah

Berbaloi membaca. Saya berpendapat alangkah bagus sekiranya kita dapat membuat investment yg membolehkan kita mendapat pulangan yg mencukupi bagi monthly expenses. Wujudkah skim2 seumpamanya ? Apa pendpt tuan.

Terima kaseh Zulkifli kerana luangkan masa untuk membaca. Saya sangat hargai.

Saya cadangkan investment di tempat yang stabil seperti ASB, unit trust, Koop , ASW. InsyaAllah , capital nyer terjaga dan pulangan yang sihat.

Jika ingin invest di unit trust, saya sangat suka investment secara bulanan. Ia kurang risiko, pulangan yang sangat bagus dan bole membina asset across time. InsyaAllah

Is it wise to pay off all my housing loan while the interest rate is low.

The rentals all cover my instalments.. I’m thinking of buying another property from my EPF..

Wah.. Mohd Fauzi ni memang suka property ya 🙂

This is my view.

If the house loan is for your own stay, then it’s ok to pay off the debt.

But, if the house is for investment, and the loans are paid by the tenants, then not necessarily. It’s good to have cash for future opportunities .

If you want buy another property, I reckon 20-30% of your EPF money.

Excellent read. Too bad way too many malaysians are not aware on how to save properly. Perhaps because there is no financial planning education in school or colleges. I’m late 30s and InsyaAllah will be able to save around 2m (1m epf n 1m savings) in about 4 years time. By the time i retire i shud be able to save around 12m. However I’m not sure whether i really need that much money. Maybe i shud retire earlier once i have around 5m in savings n spend the rest of my life study important things like religion n philosophy. I’m also quite frugal n don’t really like fancy car. My Proton Exora is more than enough for me n my family. In the current economic situation, there is no job security n that’s one of the reason why we really need to live within our means, plus having 10-15% saving is crucial.

Thanks for sharing your story Hamba Allah.

You are successful in your career as well as in your financial. Indeed you’re a young millionaire. Alhamdulillah.

I love your principle. Knowledge is more important than those fancy stuff. A good example to our community.

Wish I got this advice some 10 years ago…but still very useful at least! Tq very much bro Khairul 👍

Better late than never kan Halim 🙂

Glad that you find this article useful. Alhamdulillah

Thanks for the practical advices KAB

My pleasure Hanafiah. Thanks for reading and your support.

Alhamdulillah

Salam bro Khairul,

Is it important to take up medical card for my teenage child, since I do not have medical coverage anymore since retired?

Wasalam Rozita,

My view, priority shall be you to have your own medical card. At least, less worry of your health during retirement. Then, only for your kids.

Take care of yourself first. It will put you in a better position to support those around you. InsyaAllah

btw, saya pompuan .hehehe

Salam Khairul,

Based on our communication, at least I have the comfort that I am on right track and financially healthy in my retirement age now. Keep up the good work and bakti.

Wasalam Muzafar,

Yes, indeed you did great on your retirement fund. Alhamdulillah.

Thanks for reading and your kind words.

Enjoy your retirement. Wish you kesihatan yang terbaik and beautiful moments with family, friends and lovely grandkids. Amin.

Assalamulaikum khairul. Terima kasih dengan info yg diberi. At least Ada jgk panduan utk Saya@kita utk Masa Akan datang.. masih berbakti kurang 20 thn lagi utk bersara, in shaa Allah.. Akan dilaksanakn mengikut perancangan.. terima kasih..

Waalaikumsalam Muhamad Ismail,

Syukur sedikit sebanyak tulisan ini memberi faedah kepada Muhamad Ismail dan pembaca lain. Alhamdulillah.

Jika ingin lebih informasi dan pertolongan untuk merancang kewangan, saya sedia membantu. InsyaAllah.

Salam Ramadhan.

Good advice. What about buying a house. Buy cash using half of your EPF. House price normally increases over time. If you need money one day, sell it off.

Thanks Nazri.

Buying house for investment has it’s own challenges. With current housing price, it might and might not increase after a few years. Many factors to consider before buying a house, such as location, maintenance, impact of mistakes etc. Plus, investment in a house is not as liquid as ASB, ASW or unit trust.

If you want to buy a house, I recommend to use 20% of your EPF money.

Thanks Nazri.

Buying house for investment has it’s own challenges. With current housing price, it might and might not increase after a few years. Many factors to consider before buying a house, such as location, maintenance, impact of mistakes etc. Plus, investment in a house is not as liquid as ASB, ASW or unit trust.

If you want to buy a house, I recommend to use 20% of your EPF money.

Very important tips shared by Khairul. I find it very easy to understand and very practical too. Continue to share your view with regards to financial

Thanks so much Saravanan for your supports. Glad that you find it useful.

I truly appreciate you.

Alhamdulillah. Great to read it as I’m reaching near 55yrs and still thinking what to do with the $. Thank you for sharing and will contact you personally for some advise in shaa Allah

Terima kaseh Nor Azizah. I’m happy to know that this article gives a bit guideline to you and the readers. Alhamdulillah.

Ada rezeki in future, kita jumpa. InsyaAllah.

Salam khairul,

Tq for great tips, anyway as a muslim we should not too worry about the money, we should allocate certain % of the saving for infaq/sadakah for jariah.

Wasalam Mohamad,

Indeed true . Tangan yang memberi lebih baik dari yang menerima. When we take care of ourselves, we can provide better for the people around us. InsyaAllah.

someone approach me to invest in Islamic redeemable preference shares which gives out 12%pa

That’s seems like safe & comfortable investment do you think?

Thanks Fauzi for a great question.

My view:

1. Redeemable preferences shares (RPS) can be seen like a bond or fixed income. It pays dividend but no capital gain.

2. Instead of taking loans, company issue RPS to raise money.

3. Question to ponder: With current borrowing rate is so low at 4%, why the company would want to issue RPS and pays dividend at 12% pa?

It’s really great, appriciated

Thank you Mansoor Malik. Glad that you like it.

Thank you Mansoor Malik.

Very good points. Thank you very much.

Thanks Amiruddin for reading and your kind words. Appreciate it.

Thanks Khairul for shared your though. I just reached 55 last month. What’s your opinion if I just let my saving inside epf instead of invest in ASB, ASW or mutual fund. Might be I just need to transfer some amount into THaji. For info, I plan to continue working for next 3 years.

Alhamdulillah.. Kalau ada rezeki untuk bekerja, teruskan. Till age 60 pun ok 🙂

And you can leave your money in EFP without needing to transfer them. If you do that, then every year just withdraw about 5-7% of your total epf money.

InsyaAllah, the EPF money will last you for many many years.

Great article, thank you.

Thank C.E Tan.

Glad that you like it.