This post is for people who are looking to get their retirement sorted out. I’m going to talk about what is PRS (Private Retirement Scheme), how it works, and why you should be using one.

This will give you some information so that you can make an informed decision on whether or not this type of retirement investment is right for you.

This post has more than 1,000 words. If you know which area or topic to zoom, then make use of the table of content below. Otherwise, sit back, relax, and enjoy the insights.

Table of Contents

What is Private Retirement Scheme?

Private Retirement Scheme ( PRS ) is a retirement savings scheme that helps you to save more for retirement. It is a voluntary long-term investment to complement your EPF savings.

PRS is not mandatory and guaranteed by the Government of Malaysia like EPF (Employees Provident Fund). Plus, it does not cover under PIDM.

Like other investments, PRS is also exposed to risk and subject to market volatility. Hence, your capital or returns from this investment are not guaranteed.

However, The guidelines such as ‘The Capital Market and Service Act 2007’ and ‘Guideline on Unit Trust Funds’ provide regulatory guidance to protect the investors from theft or fraud. Hence, investor’s money remain safe.

Plus, PRS funds are managed by professional teams. The risk is reduced with the diversification of companies invested, instead of betting on a single stock.

As a consultant, I have met many people aged 50s and retirees. One of the questions I sometimes ask is how much is their EPF savings vs their last withdrawn salary.

From this exercise, I would be able to advise them on how much they can spend monthly and how to sustain their wealth during retirement. And, from that information as well, below is my finding;

If a person has only EPF savings when he retires, the dividend gain from EPF (in terms of monthly) is about 25 – 30% of his monthly salary.

Based on the above, I strongly believe every person needs to complement EPF money with their own personal savings. And, one way to build up retirement savings is by investing in PRS.

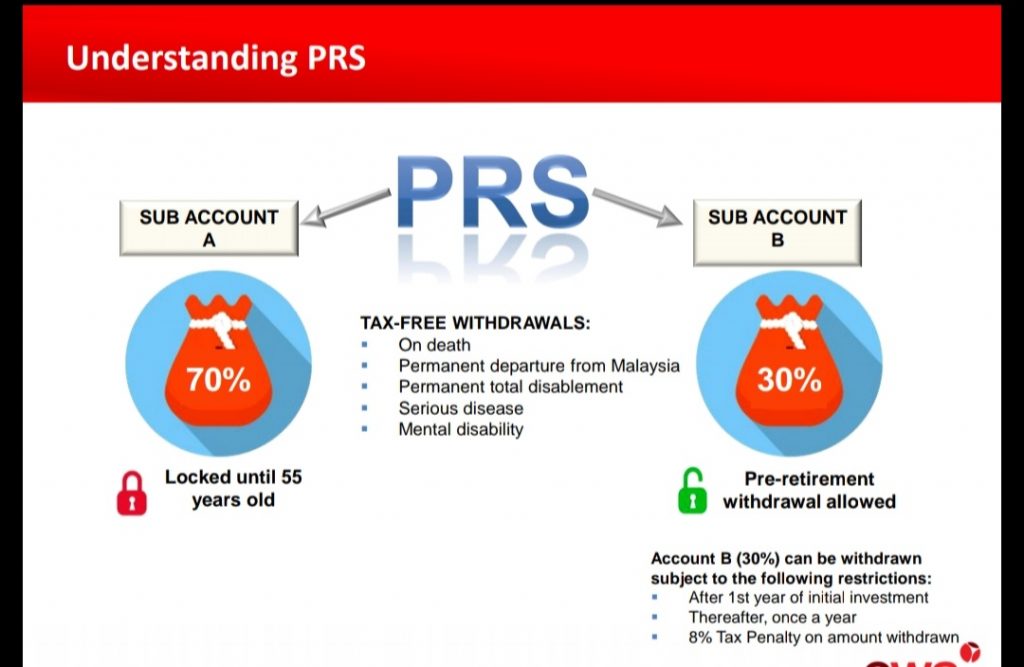

You can only withdraw money from your PRS account once you reached age 55 without any penalties.

If you want to withdraw it before age 55, you can do it from Sub Account B (30% of PRS savings) with a tax penalty of 8%. Besides that, you can only withdraw it once a year.

There are about 58 funds provided by the 8 Companies. You can invest in one or more funds or companies of your choice.

If you are not familiar with the investment, then you can opt for the default Core which will determine your funds automatically based on your age group.

For those who understand basic investing and able to manage own investment, you can invest in any of the Non-Core funds. The returns might be higher, but it’s exposed to market risk.

What is funds’ performance?

a.From the past 5 years, in general, Non-Core funds have performed the best with average annual returns of 8.24%,

b.The Core funds performance are range at annual returns of 4.07% to 7.93% (depending the type of Core group)

Source: PPA. Note that past performance is not an indicator of future performance

Most of the funds have had positive returns in the past 5 years. However, you need to choose the right fund in order to get a healthy return compared to EPF. Should you choose the wrong funds, you may risk losing your money or growing it at a slower rate.

If you want to invest in PRS, what is the best way to do it?

The good thing about a monthly contribution is the ‘dollar cost averaging concept. If the market drop, you will purchase the unit at a lower fund’s price. If the market increases, you benefit from the capital gain.

*Note: As I am a consultant registered with Principal, my preference is towards Principal’s product.

Final Thought

With starting a PRS and retirement plan , you can take control of your future financial health and retire comfortably so that all those other goals will become a reality.

Investing involves substantial risk as well as reward; readers are encouraged to do their own research before arriving at any conclusions based solely on materials provided or republished here. Read full disclaimer.