Budget is a basic and effective skill in financial planning. Budget summarises the expenses of your money or measurement of your finances.

A good analogy of budget is like you bake a cake. There are measurements for every ingredient such as sugar, flour, butter, etc.

If you put the flour too little, then the cake would not rise nicely. But if you put too much flour, the cake will end up ‘bantat’ (too hard).

The same goes for your finances. Below I share:

A Simple Guide to Budget Money That Hugely Improves Your Finances

Why should you have a budget?

A budget helps you gain control over your money. It’s also an important tool that can help you monitor and feel good about your finance

A proven budget method – Money Jar system

There are many ways to do budgeting and it’s important to find the one that works best for you. My favourite budgeting method is Money Jar System. It is simple, clear, and easy to implement.

This Money Jar System I learned during T Harv Eker seminar back in the year 2010. It was a simple and yet effective money management method. I used the system and saw a good result in my life.

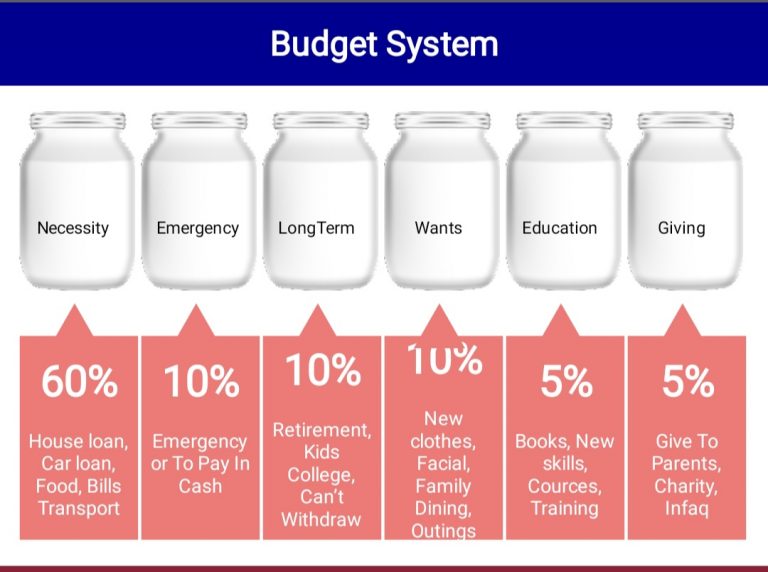

In this system, the money from your income will be divided into 6 jars which each jar represents. Ie;

60% – Necessities Jar

10% – Emergency / Pay in cash Jar

10% – Long-term / Investment Jar

10% – Wants Jar

5% – Education Jar

5% – Giving Jar

A quick illustration as below;

Let’s get through each budget jar in detail;

First Jar: Necessities (60%)

Necessities jar is your living jar. The maximum shall be 60% of your net income. The expenses in this Necessities Jar are all the expenses or commitments that you need to pay every month.

It includes;

·Food

·Home payment – mortgage, home loan or home rental

·Loans – car loan, personal loan, cash reward loan

The second jar is for Emergency or Pay In Cash. The money that you save in this jar will help you to be prepared for the unexpected as well as to get rid of the habit of getting into debt. You can buy things without simply swiping the credit card and then worry about the bill.

The purpose of this jar is to be discipline in savings and keep your money for future expenses. It’s about 10% of your monthly income. Since this is for the long term, I would encourage you not to simply spend or withdraw the money. The savings that you build in this jar shall be kept until you achieve the goals that you set such as;

You work hard every day and every month. Hence, you need to enjoy, entertain and indulge yourself. This Wants Jar will motivate you to save money as well you to have fun with in your means or sometimes to do things a bit luxurious.

Example includes:

·Buy new clothing, shoes, bags

·Outings with family

·Family dining at good restaurants

·Spa, facial or body massage

·Experience a helicopter ride

·Staycation or vacation at executive suite

Fifth Jar: Education (5%)

The fifth jar is called Education Jar. This money is for your personal and professional growth. The knowledge and skills that you acquire will make you more confident, improve your personality and quality of life.

You can spend the money in Education Jar for items;

·Books

·Courses

·Learn new skills – swimming, sewing, baking

·Career skills – public speaking, coding, writing

·Passive Income seminars – Property, Entrepreneurship, etc

The final jar is the Giving Jar. As you manage your finances better, it’s good to have the money to help others. You can give money to parents, a donation to any charity that you like, Infaq, etc

‘Tangan yang memberi lebih baik dari yang menerima’ (It’s better to give than to receive).

What if my necessity more than 60% of my income?

This is common. 70% of people living paycheck to paycheck according to a study.

When you start the budgeting plan, you might realize that your necessity is more than 60%. Don’t get discouraged by it. The Money Jar System is an ideal budget. Hence, your aim is to achieve it in the future. Just take one step of the time.

If your necessity is more than 60%, you can do 2 things;